Welcome to our new web site!

To give our readers a chance to experience all that our new website has to offer, we have made all content freely avaiable, through October 1, 2018.

During this time, print and digital subscribers will not need to log in to view our stories or e-editions.

"Exceptional." Depending on one's frame of mind, the word may conjure up anything from a mint condition rookie card to possibly being asked, again, to stay after class. But in the world of credit, exceptional refers to nearly a quarter of consumers with FICO Scores of 800 or higher. Hardly an exclusive club, but a nice place to be nonetheless.

As part of a review of consumer credit and debt among U.S. consumers, Experian looked at trends of those who had exceptional credit scores in 2023. To get to the bottom of what, exactly, exceptional credit looks like in practice, we'll highlight some of the many characteristics of the consumers behind those scores.

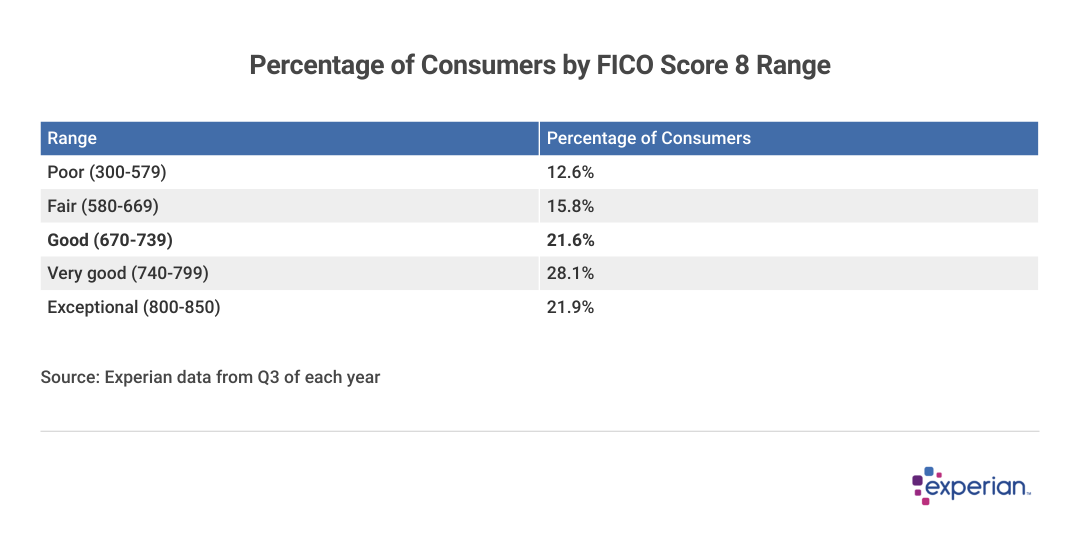

To set the stage: Most Americans have at least good credit, which is defined as a FICO Score of 670 to 739. These consumers are likely to be approved for many types of credit, but the interest they'll pay on their debt will still vary greatly.

But according to Experian data captured as 2023 came to a close, nearly 22% of consumers have a FICO Score in the highest credit score range—800 to 850. Consumers with scores in this range are considered to have exceptional credit.

Before we get into what sets these consumers apart, however, let's go over the factors that flow into a FICO Score calculation. FICO Scores are calculated based on the information in the credit reports maintained by the three credit bureaus—Experian, TransUnion and Equifax. The factors that impact FICO Scores (and how their impact is weighted) are as follows:

While factors such as income and employment status can play a role in credit approval, they don't have a direct effect on credit scores.

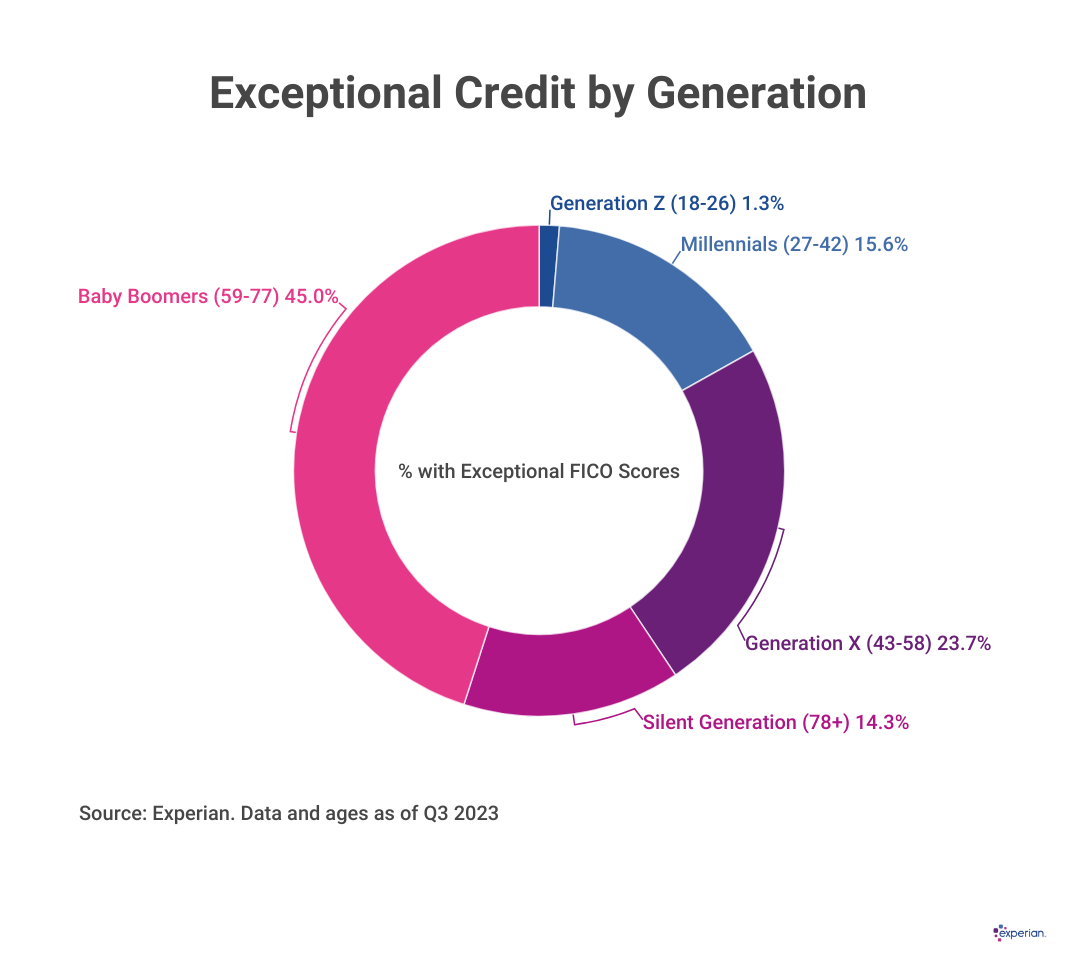

Nearly half—45%—of consumers with exceptional credit are baby boomers, even though boomers represent only about one-fifth of consumers. The likelihood of older generations having exceptional credit shouldn't be a surprise: Length of credit history is an important factor in calculating a FICO Score.

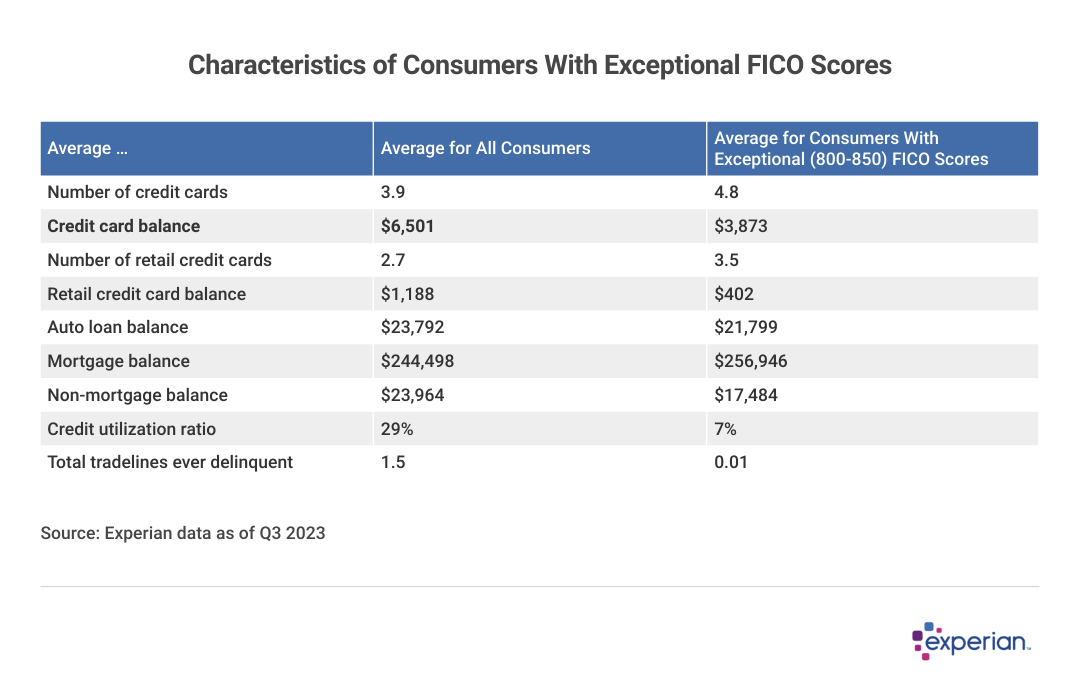

There were some distinct differences that stood out when comparing overall consumer averages against average stats for consumers with exceptional credit scores. Of particular note among the two measures of consumers was the number of delinquencies (late payments). While a typical consumer has one or two delinquencies on their credit report, those with a FICO Score of 800 or greater have virtually zero delinquencies among them.

Otherwise, the characteristics of a consumer with exceptional credit mimics that of more seasoned consumers: They have more lines of revolving credit on average, but much lower average revolving balances. A virtuous consequence of low credit card balances is often a lower credit utilization ratio, which is a key credit score factor. Those with an exceptional credit score have average utilization ratios under 10%, versus 29% for the average consumer. Lower utilization ratios—those in the single digits—can have a positive effect on FICO Scores.

Borrowers with exceptional credit scores also carry a slightly larger average mortgage balance than the average consumer, as well as a slightly lower balance on any auto loans in their names.

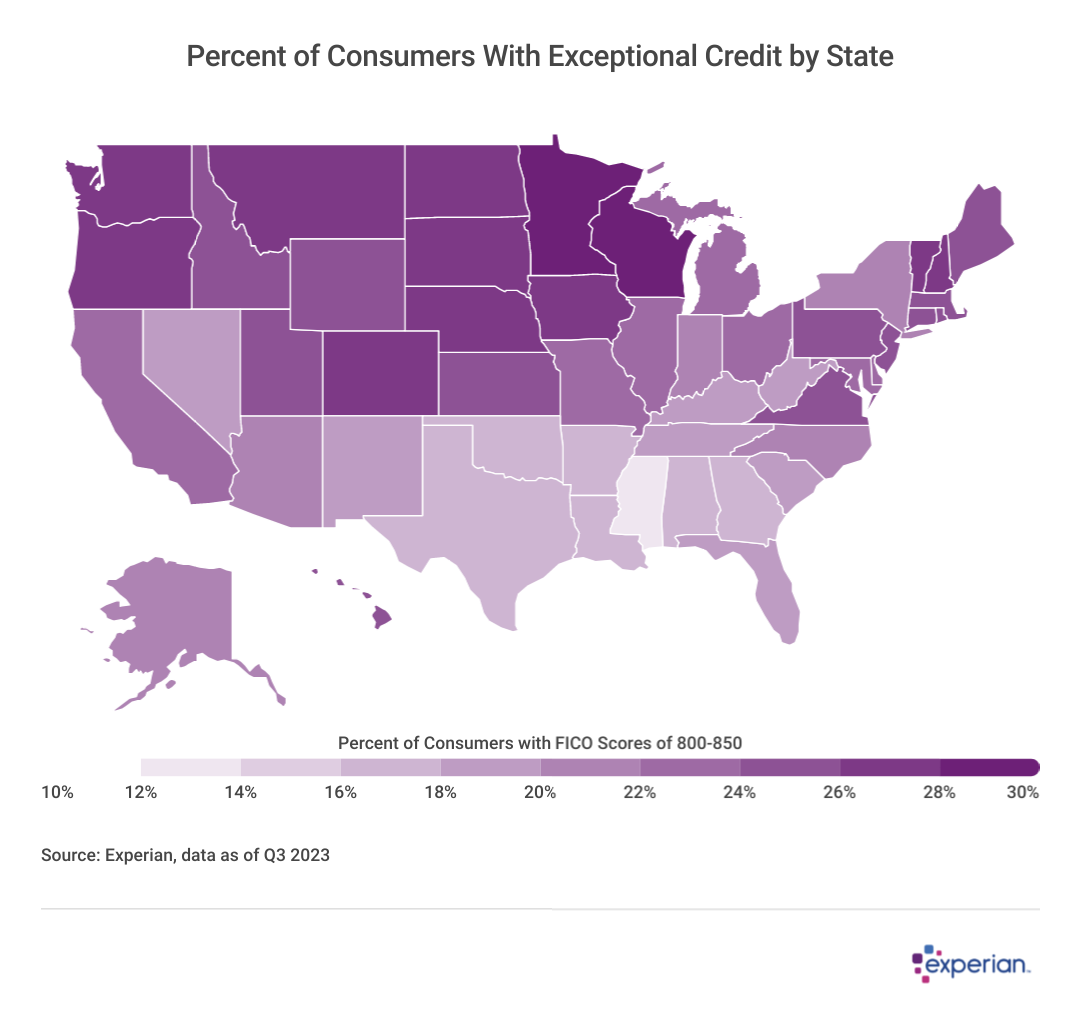

Above-average may be selling Minnesotans short—nearly one-third of state residents have an exceptional credit score. The Gopher State, alongside their Badger State neighbors in Wisconsin, lead the nation with the highest percentage of consumers with an 800 or better FICO Score. State mascots aside, there is a decidedly Northern tilt to where consumers with exceptional credit scores reside.

Rounding out the five states with the highest percentages of exceptional credit scores are New Hampshire, North Dakota and Vermont.

What Exceptional Credit Can Earn Consumers

According to FICO, exceptional scores indicate that "your score is well above the average score of U.S. consumers and clearly demonstrates to lenders that you are an exceptional borrower." In practice, consumers with exceptional credit are more likely to receive approval for most types of credit—often with accompanying lower interest rates—than other consumers.

Nonetheless, even consumers with exceptional credit won't necessarily receive approval for big-ticket items, like a new home, if other lender criteria aren't met. With mortgage APRs hovering close to 7% in 2024, lenders want to be certain that a borrower's income is sufficient to cover monthly homeowner expenses, even if they do have exceptional credit.

This story was produced by Experian and reviewed and distributed by Stacker Media.